EN

EN  ES

ES PT

PTThe Challenges of the Value Chain for Renewable Energy Companies

The electricity sector plays a key role in global efforts to mitigate the rise in Earth’s temperature. Many companies are looking to diversify their energy generation with renewables to lead the transition to a low-carbon economy. However, renewable energy companies face a challenge: how to expand their generation while supporting other sectors in the energy transition without increasing the indirect emissions associated with their operations?

The Global and Brazilian Electricity Sector

According to the WRI Climate Watch¹ initiative, the electricity sector is responsible for the highest direct emissions compared to other sectors, accounting for approximately 30% of global emissions in 2019. This is due to the global electricity generation matrix is composed of 73% non-renewable sources, relying mainly on coal and natural gas, according to the IEA publication of 2021², .

On the other hand, the Brazilian Electricity Sector (BES) has a predominantly renewable energy matrix. In 2022 it reached its highest milestone in the past 9 years, with 87% of renewable energy in the total energy generation. In the same year, over 60% of Brazil’s electricity came from hydroelectric plants, and wind power became the second most important source of electricity generation, surpassing the combined generation of thermal, natural gas, coal, and oil-derived sources for the first time.

According to Climate Watch, the Brazilian Electricity Sector is only the fourth largest emitter of greenhouse gases (GHGs) in Brazil, with emissions from deforestation, agriculture, and transport being more significant contributors. Emissions from electricity and steam production accounted for approximately 7% of national emissions in 2019.

Scope 3 Challenges

The low reliance on fossil fuels in Brazilian electricity generation shifts the materiality of emissions to the value chain. For renewable energy companies, the upstream emissions prior to electricity generation can account for almost all of the company’s emissions. In addition, the increasing demand for electricity³, especially from less emission-intensive sources, leads to higher indirect emissions associated with equipment, infrastructure, and construction of renewable generation facilities.

In this context, mapping, quantifying and reducing Scope 3 emissions⁴ is strategic for companies in the sector to make robust climate commitments, following reference initiatives such as the Science Based Target Initiative. However, managing Scope 3 emissions requires overcoming a number of complexities due to the distance between the company and the major emission sources, and the influence over various actors in the supply chain.

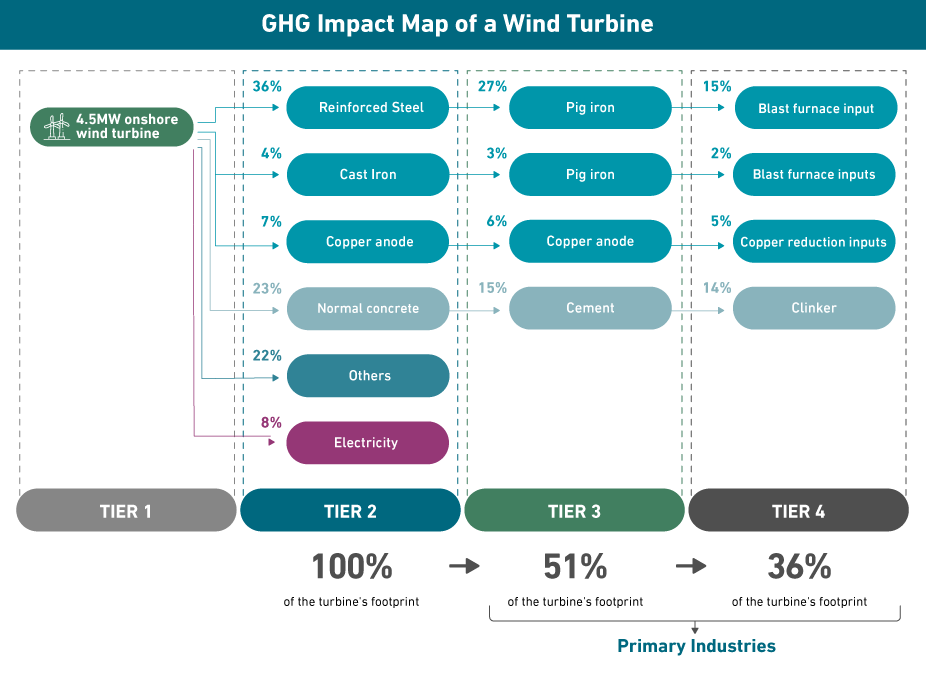

The supply chain can be divided into tiers, according to their proximity to the company. Tier 1 suppliers are the direct suppliers, while Tier 2 includes the suppliers of the direct suppliers, and so on. For example, in the life cycle of a wind turbine, more than 50% of the emissions are located in Tier 3, i.e. in the suppliers of the primary industry, such as steel and cement manufacturers5.

Our Solutions

Against this backdrop, WayCarbon has developed a strategic and comprehensive approach to address complex supply chain challenges. Based on recognised guidelines, the journey begins with the technical mapping of suppliers and critical consumer goods, along with the development of measurement methodologies for chain reductions, such as insetting programs, while keeping the strategic objective in mind.

The complete solution consists of four facilitating axes to build a common narrative, where the company, suppliers and various stakeholders can radically collaborate to increase data reliability and traceability, and promote decarbonization opportunities in the supply chain. The approach supports regionalization by strengthening innovative initiatives and advocating for structural solutions, as well as continuously monitoring progress to achieve deep and systemic change.

References

¹ Available at <https://www.climatewatchdata.org>

² Available at <https://www.iea.org/data-and-statistics/charts/global-electricity-generation-mix-2010-2020>

³ Brazil’s per capita electricity consumption is relatively low compared to countries such as Germany, France, Australia and the US, and therefore has room for growth (https://data.worldbank.org/indicator/EG.USE.ELEC.KH.PC). In addition, the advancement of the global climate agenda relies on the electrification of end use (IEA 2022), Electrification, IEA, Paris https://www.iea.org/reports/electrification, License: CC BY 4.0)

⁴ Indirect emissions resulting from the organization’s activities but occurring at sources controlled by third parties.

5 Analysis made from the Ecoinvent emission factor “wind turbine construction, 4.5MW, onshore – GLO – wind turbine, 4.5MW, onshore”, database 3.9.1, IPCC 2021 method.

Luisa Gonzaga

Caroline Botta